Japan's 2026 Shunto Delivers 5.01% Wage Rise for Third Year

**Keywords:** Japan shunto 2026, Rengo wage survey, SME wage gap, labor shortages Japan, BOJ rate hike, real wage growth, Keidanren Tsutsui, Akira Nidaira, defensive wage increases, CPI inflation Japan Final Shunto Results The Japanese Trade Union Confederation, known as Rengo, released its final survey results on July 3, 2026, confirming an average wage increase of 5.01 percen

Final Shunto Results

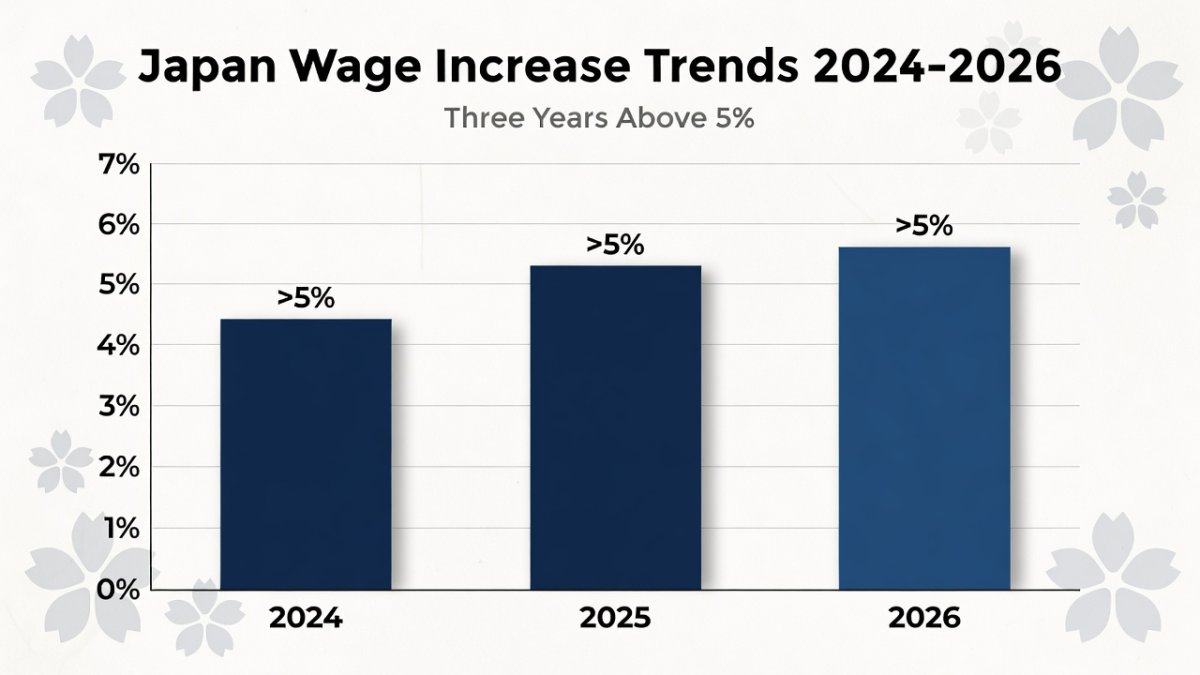

The Japanese Trade Union Confederation, known as Rengo, released its final survey results on July 3, 2026, confirming an average wage increase of 5.01 percent across affiliated unions. This figure combines pay scale adjustments and regular salary hikes, translating to an average monthly gain of 16,400 yen. The outcome marks the third consecutive year in which the weighted average has exceeded the 5 percent threshold, following similar results in 2024 and 2025.

The survey encompassed 5,368 Rengo-affiliated companies and reflected a modest decline of 0.24 percentage points from the 5.25 percent recorded in 2025. Despite the slight dip, the results met Rengo's stated target of at least 5 percent overall. Preliminary data released in March had shown a higher 5.26 percent, but the final revision incorporated additional information from smaller enterprises that pulled the average downward.

These outcomes underscore a sustained shift in Japan's wage landscape after decades of stagnation. The consistent achievement above 5 percent for three years signals that base-pay increases have become more normalized across the economy. Senior Rengo officials noted that the latest round demonstrates measurable progress toward establishing a society where annual wage hikes are routine rather than exceptional.

Analysts emphasize that the 5.01 percent result occurred against a backdrop of structural labor market tightness. The weighted average calculation gives greater influence to larger firms, yet the overall figure still reflects broad participation from Rengo members. This continuity in high-single-digit percentage gains provides a foundation for further discussions in subsequent negotiation rounds.

SME Performance Gap

Small and medium-sized enterprises with fewer than 300 employees recorded an average wage increase of 4.69 percent, equivalent to 12,866 yen per month. This result represented a marginal improvement of 0.04 percentage points compared with 2025, yet it remained well below Rengo's separate 6 percent target set specifically for smaller unions. The gap between SME outcomes and the overall average highlights persistent disparities in bargaining power and financial capacity.

Smaller unions account for approximately 70 percent of total employment in Japan, making their performance critical to the broader wage picture. Many of these unions operate in sectors with thinner profit margins and limited ability to absorb higher labor costs without corresponding revenue growth. The shortfall relative to the 6 percent target illustrates the challenges these organizations face when competing for talent against larger corporations that can more readily offer substantial raises.

Rengo officials have repeatedly stressed that closing this SME gap will require targeted policy support and improved productivity measures. Without such interventions, the divergence risks entrenching a two-tier labor market where workers at smaller firms continue to experience slower income growth. The 4.69 percent figure, while positive, underscores the need for continued focus on smaller enterprises in future shunto rounds.

Data from the survey indicate that SMEs have made incremental progress, yet structural constraints limit their ability to match larger firms. This performance gap carries implications for overall consumption patterns, as the majority of Japanese workers are employed by these smaller entities. Sustained efforts to narrow the divide remain essential for achieving economy-wide wage momentum.

Sectoral Dynamics and Labor Shortages

Leading gains in the 2026 shunto negotiations emerged from the passenger and goods transport, commerce, and logistics sectors. These industries have faced acute labor shortages, prompting employers to offer more competitive compensation packages to attract and retain workers. The concentration of stronger wage outcomes in these areas reflects the direct impact of demographic and economic pressures on specific segments of the economy.

The Bank of Japan Tankan survey for March 2026 reported a diffusion index of minus 38 for employment conditions, marking one of the highest levels of perceived understaffing in recent history. This reading underscores the severity of labor shortages across multiple industries and helps explain why transport and logistics firms led the wage increases. Companies in these sectors have had to respond aggressively to maintain operational capacity amid declining availability of younger workers.

Japan's plunging birth rate has further reduced the supply of new entrants into the workforce, intensifying competition for available labor. Large corporations in shortage-prone sectors have raised wages partly to improve recruitment outcomes, and SMEs have been compelled to follow suit to remain competitive. This dynamic has created upward pressure on compensation levels even in industries traditionally characterized by modest pay growth.

The sectoral pattern observed in the Rengo data illustrates how labor market imbalances can drive wage outcomes more effectively than traditional bargaining power alone. Transport and logistics firms, facing immediate operational constraints, prioritized wage adjustments to secure necessary staffing. This trend is expected to persist as demographic headwinds continue to constrain labor supply in the coming years.

Management and Union Alignment

Keidanren Chairman Tsutsui Yoshinobu stated that management should begin wage discussions from the premise of an increase in base pay. This position reflects a notable evolution in employer attitudes compared with previous decades when resistance to regular base-pay hikes was more common. The statement signals greater acceptance among business leaders of the need for sustained wage growth to support economic vitality.

Rengo senior official Akira Nidaira commented that the latest increases confirm further progress toward a society in which wage hikes are common. His remarks highlight the union confederation's view that the 2026 results represent incremental but meaningful advancement in establishing a new norm for annual compensation adjustments. The alignment between Keidanren's stance and Rengo's assessment suggests a degree of consensus between labor and management on the direction of wage policy.

Both sides have recognized that proactive wage increases can help address recruitment challenges and support consumer spending. Large firms have taken the lead in implementing base-pay raises, creating competitive pressure that extends to smaller enterprises. This shared recognition has contributed to the third consecutive year of results above 5 percent despite varying economic conditions across firms.

The convergence of views between major business organizations and labor unions provides a foundation for continued dialogue in future negotiations. While differences remain regarding the pace and distribution of gains, the public statements from Tsutsui and Nidaira indicate a mutual interest in sustaining wage momentum. This alignment may prove important as Japan navigates ongoing demographic and inflationary challenges.

The Defensive Wage Problem

Approximately 35.5 percent of SMEs reported raising wages defensively even though their business conditions had not improved. These increases often stem from the necessity to retain workers amid severe labor shortages rather than from stronger revenue or productivity performance. Such defensive adjustments place additional strain on companies already operating with limited financial flexibility.

Many smaller firms face difficulties passing higher labor costs on to customers, particularly in competitive markets where price sensitivity remains high. This constraint contributes to a situation in which wage growth outpaces improvements in business fundamentals for a significant share of employers. The result is a growing number of SMEs exiting the market when they cannot adapt to the new wage environment.

Japan's labor share of income has continued to decline even as nominal wages rise, indicating that wage increases have not kept pace with productivity gains in recent years. This trend raises questions about the sustainability of current wage momentum if underlying productivity improvements do not accelerate. Defensive wage hikes may temporarily address labor shortages but do not resolve deeper structural imbalances in income distribution.

The prevalence of defensive increases among SMEs highlights the uneven nature of Japan's economic recovery. While larger firms can more easily absorb higher labor costs, smaller entities often lack comparable pricing power or operational scale. Addressing this disparity will require both policy measures and business strategies aimed at enhancing productivity across the SME sector.

Real Wage Recovery

The 2026 shunto results contributed to the first positive real wage growth recorded in 26 months. This development marks a significant turning point after an extended period in which inflation eroded nominal wage gains. Real wage improvements provide workers with greater purchasing power and support broader consumption trends within the Japanese economy.

Japan's consumer price index has remained above 2 percent since 2022, reflecting a sustained shift from a deflationary to an inflationary environment. Food and energy price increases, driven by global factors including Middle East conflict and climate-related disruptions, have been primary contributors to this inflationary pressure. The transition has altered the context in which wage negotiations occur, making real wage preservation a central concern for unions.

Despite the positive real wage reading, the pace of recovery remains modest relative to the cumulative losses experienced during the preceding period. Workers continue to feel the effects of elevated living costs, particularly in essential categories such as food and housing. Sustained nominal wage growth above inflation will be necessary to build on the initial real wage improvement observed in 2026.

The emergence of positive real wage growth coincides with broader economic adjustments, including efforts by firms to pass through higher costs where possible. This development offers cautious optimism that the cycle of wage stagnation may be giving way to more balanced income dynamics, provided inflation pressures do not accelerate further.

BOJ Policy Implications

Market participants assigned a 93 percent probability to an additional Bank of Japan rate hike following the release of the final Rengo survey data. The combination of sustained wage growth and persistent labor shortages has strengthened expectations that the central bank will continue normalizing monetary policy. This outlook reflects the view that wage momentum supports the case for gradual tightening.

The Bank of Japan has emphasized the importance of establishing a virtuous cycle in which wage increases and price stability reinforce each other. The 2026 shunto results provide evidence that such a cycle may be taking shape, particularly in sectors experiencing acute labor shortages. Policymakers will monitor whether these gains extend more broadly across the economy in subsequent negotiation rounds.

Demographic pressures, including Japan's declining birth rate and shrinking workforce, continue to influence both wage outcomes and monetary policy considerations. Labor shortages have become a structural feature that supports higher compensation levels, yet they also pose risks to long-term economic growth if left unaddressed. The BOJ's policy decisions will need to account for these demographic realities alongside inflation and wage trends.

Additional rate hikes carry implications for borrowing costs and investment decisions across Japanese businesses. While the probability of further tightening has increased, the pace and magnitude of any adjustments will depend on incoming data regarding wage growth, inflation, and overall economic performance. The 2026 shunto results have added an important data point to this ongoing assessment.

Outlook

Looking ahead, Japan faces ongoing challenges in sustaining wage momentum amid persistent global inflationary pressures on food and energy. These external factors complicate efforts to maintain real wage gains and require continued vigilance from both policymakers and businesses. Structural reforms aimed at boosting productivity, particularly among SMEs, will be essential to support further compensation increases.

The gap between large firms and smaller enterprises remains a key area requiring attention. Without targeted measures to enhance SME competitiveness and profitability, the benefits of higher wage growth risk remaining unevenly distributed. Closing this divide will help ensure that the majority of Japanese workers participate in the emerging wage recovery.

Demographic headwinds, including the declining birth rate and resulting labor shortages, will continue to shape wage negotiations in future years. Sectors such as transport and logistics are likely to remain at the forefront of compensation adjustments as they compete for a shrinking pool of available workers. Broader policy responses will be needed to address these long-term supply constraints.

Overall, the 2026 shunto results represent meaningful progress while highlighting areas that require further action. Continued alignment between labor and management, combined with supportive policies, offers the best prospect for building on the gains achieved in recent years. The coming negotiation rounds will test whether the current momentum can be maintained and extended across the economy.

Tags: Japan shunto 2026, Rengo wage survey, SME wage gap, labor shortages Japan, BOJ rate hike, real wage growth, Keidanren Tsutsui, Akira Nidaira, defensive wage increases, CPI inflation Japan

By Kenji Tanaka, Staff Writer

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Japan Correspondent at Global1.News. Tokyo-based voice covering Japanese politics, technology, economy, and culture. Tracks the intersection of tradition and innovation in one of the world's most dynamic societies.

Comments (0)